TholaCash Blog

Financial education, budgeting tips, and smart borrowing guidance.

Online Finance Fraud in South Africa: How to Protect Yourself

Online Finance Fraud in South Africa: How to Protect Yourself As more financial services move online, criminals are finding new ways to scam unsuspecting consumers. Online finance fraud is rising in South Africa, affecting people who apply for loans, use online banking, or respond to financial offers on social media. Understanding how these scams work is the first step in protecting yourself. What Is Online Finance Fraud? Online finance fraud happens when criminals use the internet to trick people into: Sharing personal information Sending money Paying fake “fees” Clicking malicious links Providing banking details Fraudsters often impersonate legitimate lenders, banks, or financial institutions to appear trustworthy. Common Online Finance Scams 1. Fake Loan Approval Scams You receive a message saying you’ve been “pre-approved” for a large loan. Before receiving funds, you’re asked to pay: An upfront fee Insurance cost “Processing” charge Admin fee Once payment is made, the scammer disappears. Red flag: Legitimate lenders do not ask for upfront payment before disbursing a loan. 2. Phishing Emails and SMS Scammers send messages pretending to be from your bank or a financial provider. These messages often say: “Your account has been compromised.” “Verify your details urgently.” “Click here to avoid suspension.” The link leads to a fake website designed to steal your login details. 3. Social Media Impersonation Fraudsters create fake profiles pretending to represent legitimate lenders. They use: Company logos Fake testimonials Stolen website content They then request personal documents or payments via private message. 4. WhatsApp Loan Scams You may receive a WhatsApp message offering “instant approval” with no credit checks. These scammers often request: Copies of your ID Bank statements Upfront “release fees” After receiving documents or money, they disappear — or misuse your information. The Risks of Online Financial Fraud Online fraud can result in: Loss of money Identity theft Unauthorized bank transactions Damaged credit profile Emotional stress Recovering from fraud can take months and may involve lengthy disputes with banks and authorities. How to Protect Yourself Here are simple steps to stay safe: ✅ Verify Before You Trust Always confirm that the lender is registered and has a legitimate website and official contact details. ✅ Never Pay Upfront Loan Fees Legitimate lenders do not require upfront payments before releasing funds. ✅ Check Website URLs Carefully Look for: HTTPS security Correct spelling Professional design Contact details that match official listings ✅ Protect Your Personal Information Never share: Banking PINs OTP codes Passwords Card CVV numbers Even a “support agent” should never ask for these. ✅ Contact the Company Directly If you receive a suspicious message, contact the company using the phone number listed on their official website — not the number in the message. What To Do If You’ve Been Scammed If you suspect fraud: Contact your bank immediately. Change your passwords. Report the scam to relevant authorities. Monitor your credit profile. Acting quickly can reduce the damage. Final Thoughts Online financial services are convenient — but convenience should never replace caution. Before applying for any loan or sharing personal information online, take a moment to verify: Is this company legitimate? Are they asking for upfront fees? Does the website look secure? Financial awareness is your first line of defense against fraud. Stay informed. Stay cautious. Stay protected.

Read More →

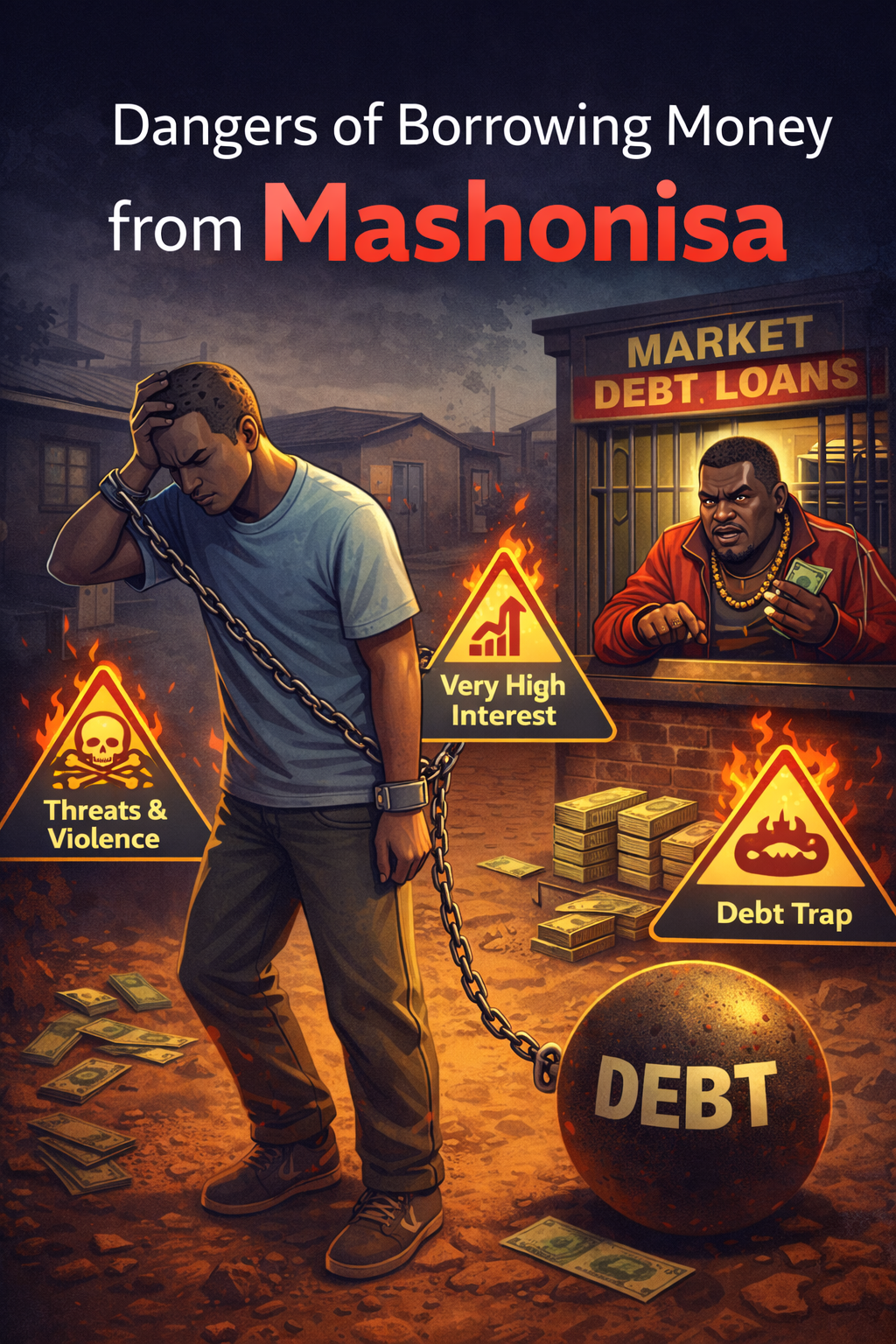

The Dangers of Borrowing from Mashonisas

1. Extremely High Interest Rates Mashonisas often charge very high interest rates, sometimes far above what is legally allowed for registered credit providers. Because these lenders operate informally, there is usually: No written contract No clear breakdown of fees No transparency on total repayment What starts as a small loan can quickly double or triple in a short period. This creates a cycle where borrowers struggle to keep up, leading to more borrowing just to repay previous debt. 2. No Legal Protection When you borrow from a registered credit provider, you are protected by South African credit laws. These laws regulate: Maximum interest rates Collection practices Your rights as a borrower Fair treatment and dispute processes Mashonisas are not regulated in the same way. If something goes wrong, you have very limited legal protection. 3. Threats and Intimidation In some cases, mashonisas use intimidation tactics to ensure repayment. These may include: Harassment Confiscating ID documents or bank cards Public embarrassment Threats of violence Even if not all informal lenders behave this way, the lack of regulation increases the risk. 4. Debt Trap Cycle Because of high interest and short repayment periods, many borrowers: Fail to repay on time Take another loan to cover the first one Fall deeper into debt each month This cycle can become extremely difficult to escape and may affect your financial stability for years. 5. Damage to Your Financial Future Borrowing from informal lenders does not help you build a positive credit profile. In fact: There is no record of responsible repayment. There is no formal affordability assessment. You may become dependent on high-cost short-term borrowing. This makes it harder to qualify for formal credit products in the future. What Should You Do Instead? If you are in financial difficulty, consider safer alternatives: Borrow only from registered credit providers. Always review the total repayment amount. Create a repayment plan before accepting any loan. Speak to a registered debt counsellor if overwhelmed. Build a small emergency fund—even R50 per week helps. Responsible borrowing protects not only your finances but also your peace of mind. Final Thoughts Quick cash can be tempting during emergencies, but borrowing from unregulated lenders can expose you to high costs, harassment, and long-term debt problems. Before taking any loan, ask yourself: Is this lender registered? Do I understand the total repayment? Can I afford to repay without borrowing again? Making informed decisions today protects your financial future tomorrow.

Read More →

How to Budget Using the 50/30/20 Rule

Managing your money doesn’t have to be complicated. One of the simplest and most effective budgeting methods is the 50/30/20 rule. It helps you divide your income into three clear categories so you can cover your needs, enjoy your lifestyle, and still build financial security. If you’ve ever wondered where your money goes each month, this method is a great place to start. What Is the 50/30/20 Rule? The 50/30/20 rule divides your after-tax income into three parts: 50% – Needs 30% – Wants 20% – Savings or Debt Repayment This structure creates balance. You cover essentials, enjoy life responsibly, and still prepare for the future. 50% – Needs (Essential Expenses) Needs are the expenses you must pay to live and work. Examples include: Rent or home loan Groceries Electricity and water Transport Insurance School fees Minimum debt repayments If your essential expenses are more than 50%, it may be a sign that your fixed costs are too high. Consider adjusting housing, transport, or subscription expenses where possible. 30% – Wants (Lifestyle Spending) Wants are things that improve your quality of life but aren’t essential. Examples: Eating out Streaming services New clothes Entertainment Gym memberships Vacations This category is flexible. If you need to save more, this is usually the first place to cut back. 20% – Savings and Debt Reduction This is the category that builds your future. It can include: Emergency savings Retirement contributions Investment accounts Extra debt repayments (beyond the minimum) If you don’t yet have an emergency fund, start here. Even saving a small amount consistently makes a big difference over time. How to Start Using the 50/30/20 Rule Calculate your monthly take-home income. Multiply it by 50%, 30%, and 20%. Track your current spending. Adjust categories to match the rule as closely as possible. For example, if you earn R10,000 per month: R5,000 → Needs R3,000 → Wants R2,000 → Savings or debt repayment It doesn’t need to be perfect from day one. The goal is progress, not perfection. Why This Method Works The 50/30/20 rule works because it’s: Simple Flexible Easy to remember Balanced It prevents overspending while still allowing room to enjoy your money responsibly. Final Thoughts Financial freedom doesn’t happen overnight. But with a structured plan like the 50/30/20 rule, you can take control of your money step by step. Smart budgeting leads to: Less stress Fewer emergencies Better borrowing decisions Stronger financial stability At TholaCash, we believe responsible financial planning is just as important as access to credit. When you manage your money wisely, you build a stronger future.

Read More →