How much do you need?

Move the slider to see your total repayment.

Pricing model used in this calculator:

- Initiation Fee: R165 up to R1,000, then formula-based increase (capped)

- Interest: 5% of principal

- Service Fee: R60

- Repayment term shown: 1 month, single installment

Final approval, quote validity, and mandate steps are confirmed in your dashboard after assessment.

What You Need to Apply

- Valid South African ID

- Active bank account

- 3 months statements OR payslips

- Email address

How to Apply

How Decisions Work

We review affordability, supporting documents, credit profile, and mandate details before making a final loan decision. If approved, you’ll receive your quote and DebiCheck mandate in your dashboard.

Customers Trust TholaCash

How It Works

A quick summary of your loan journey from application to repayment.

Submit Application

Choose your loan amount and complete your online application details.

Provide Documents

Upload required documents for identity and affordability verification.

Credit Assessment

We perform affordability and credit checks to evaluate your application.

Review Loan Quote

If approved, review your official quote and repayment terms.

Accept Mandate

Read and accept the official DebiCheck mandate in your dashboard.

Funds Disbursed

After bank mandate confirmation, funds are paid to your account.

Repayment Scenarios

Starter Example

Loan amount: R1,000

Term: 1 month

Single repayment aligned to salary date.

Mid-Range Example

Loan amount: R3,500

Term: 1 month

Quote shows full cost before acceptance.

Higher Amount Example

Loan amount: R8,000

Term: 1 month

DebiCheck confirmation required before disbursement.

Why Choose TholaCash?

Secure & Encrypted

Your data is encrypted and protected using modern security controls.

Fast Decisions

Quick assessments and streamlined digital applications.

Transparent Pricing

Clear breakdown of fees and repayment before you continue.

Compliance & Security

POPIA Compliant

Responsible Lending

Encrypted Systems

Latest from our Blog

Online Finance Fraud in South Africa: How It Happens and How to Protect Yourself

Online Finance Fraud in South Africa: How It Happens and How to Protect Yourself As more South Africans use the internet for banking, loans, and shopping, online financial fraud has become a growing problem. Criminals use technology and social engineering to trick people into sharing personal information, sending money, or giving access to their bank accounts. Understanding how these scams work is the first step toward protecting yourself and your finances. What Is Online Financial Fraud? Online financial fraud happens when criminals use the internet, mobile phones, or digital platforms to steal money or sensitive financial information. Fraudsters often pretend to be: Banks Loan providers Online stores Government institutions Investment companies They use fake websites, emails, phone calls, and social media messages to gain trust and steal money. Common Types of Online Finance Fraud in South Africa 1. Phishing Scams Phishing is when scammers send emails, SMS messages, or WhatsApp messages pretending to be from a bank or financial institution. The message usually contains a link to a fake website that looks like a real banking page. When victims enter their login details, the criminals steal the information. Common phishing messages include: “Your bank account has been suspended. Click here to verify.” “Unusual activity detected. Please confirm your details.” 2. Fake Loan Offers Fraudsters often advertise instant loans on social media or WhatsApp. These scams usually promise: Guaranteed approval No credit checks Very low interest rates Victims are then asked to pay “processing fees” or “insurance fees” before the loan is released. Once the money is paid, the scammer disappears. Legitimate lenders registered with the National Credit Regulator will never ask for upfront payments before a loan is approved. 3. Investment Scams Many South Africans have lost money to fake investment opportunities promising extremely high returns. These scams often promote: Cryptocurrency investments Forex trading platforms “Guaranteed” investment profits If an investment promises very high returns with little or no risk, it is usually a scam. 4. SIM Swap Fraud SIM swap fraud happens when criminals trick mobile providers into transferring your phone number to a new SIM card. Once they control your number, they can: Intercept banking OTPs Reset banking passwords Access your online banking accounts 5. Online Marketplace Fraud Scammers also target buyers and sellers on online marketplaces. Typical scams include: Fake payment confirmations Selling goods that never arrive Buyers sending fake proof of payment Warning Signs of Financial Scams Watch out for these common red flags: Requests for upfront payments for loans or prizes Messages creating urgent pressure to act quickly Requests for bank PINs, passwords, or OTP codes Deals that sound too good to be true Websites with no contact details or business registration Legitimate financial institutions follow strict regulations and provide clear information about their services. How to Protect Yourself from Online Fraud Never Share Sensitive Banking Information Your bank will never ask for your PIN, password, or OTP codes through email, SMS, or phone calls. Verify Financial Companies Before taking a loan or making an investment, check whether the company is registered with the National Credit Regulator or other relevant authorities. Be Careful with Links Avoid clicking links in suspicious messages. Instead, visit the official website directly by typing the address into your browser. Use Strong Passwords Protect your accounts by using: Unique passwords Two-factor authentication Secure password managers Monitor Your Bank Accounts Regularly check your bank statements and immediately report any suspicious transactions to your bank. Borrowing Safely Online If you need a loan, it is important to use trusted and regulated lenders that follow South African credit laws. Responsible lenders provide: Clear loan agreements Transparent interest rates No hidden fees Secure application processes For example, TholaCash Financial Services provides short-term financial assistance while following responsible lending practices. What to Do If You Are a Victim of Fraud If you suspect fraud: Contact your bank immediately Report the incident to the police Notify your mobile provider if a SIM swap may have occurred Change all passwords and secure your accounts Acting quickly can help prevent further losses. Final Thoughts Online financial fraud is becoming more sophisticated, but many scams can be avoided by staying informed and cautious. Always verify financial services, protect your personal information, and avoid deals that seem too good to be true. By staying alert and choosing trusted financial providers, you can protect yourself and your money in the digital world.

Read More →

How to Budget Using the 50/30/20 Rule (A Simple Guide for South Africans)

How to Budget Using the 50/30/20 Rule (A Simple Guide for South Africans) Managing money can feel overwhelming, especially when income needs to cover rent, groceries, transport, and unexpected expenses. One of the simplest and most effective budgeting methods is the 50/30/20 rule. This approach helps you organize your income into three clear categories so you can cover your needs, enjoy life, and still save for the future. Whether you earn a salary, run a small business, or receive irregular income, the 50/30/20 rule can help you build better financial habits. What Is the 50/30/20 Budget Rule? The 50/30/20 rule divides your after-tax monthly income into three parts: 50% for Needs 30% for Wants 20% for Savings and Debt Repayment This simple structure ensures your essential expenses are covered while still making room for lifestyle spending and long-term financial goals. Step 1: Allocate 50% for Needs Needs are essential expenses you must pay to live and work. These are non-negotiable costs. Examples of needs include: Rent or bond payments Groceries and basic food items Electricity and water Transport or petrol Insurance School fees Minimum debt repayments For example, if you earn R10,000 per month, about R5,000 should go toward essential expenses. If your needs exceed 50% of your income, you may need to look at ways to reduce costs, such as cutting unnecessary subscriptions or finding cheaper alternatives for certain expenses. Step 2: Allocate 30% for Wants Wants are things that improve your lifestyle but are not strictly necessary. Examples include: Eating out Entertainment and streaming services Clothing and shopping Gym memberships Holidays or weekend outings Using the previous example, if you earn R10,000 per month, about R3,000 can be spent on wants. This part of the budget allows you to enjoy your money without overspending. Step 3: Allocate 20% for Savings and Debt Reduction The final 20% of your income should go toward improving your financial future. This may include: Emergency savings Retirement savings Paying off loans faster Investments Saving for major purchases (car, home, education) With a R10,000 monthly income, R2,000 would go toward savings or paying off debt. Building an emergency fund is especially important because it helps you avoid borrowing money when unexpected expenses arise. Example Budget Using the 50/30/20 Rule Here’s what a simple budget might look like: Category Percentage Example (R10,000 income) Needs 50% R5,000 Wants 30% R3,000 Savings / Debt 20% R2,000 This structure keeps your finances balanced and prevents overspending. Tips for Making the 50/30/20 Rule Work Track your spending Before creating a budget, review your bank statements or spending history to see where your money goes. Adjust the rule if needed If your rent or transport costs are high, you may temporarily adjust the percentages while working toward better balance. Start small with savings If saving 20% feels difficult, start with 5–10% and increase gradually. Use budgeting apps or spreadsheets Digital tools can help track spending and keep your budget organized. Why the 50/30/20 Rule Works The biggest advantage of this budgeting method is its simplicity. Instead of tracking dozens of categories, you only manage three main areas of spending. It helps you: Avoid living paycheck to paycheck Build savings consistently Reduce financial stress Maintain a healthy balance between spending and saving Final Thoughts Budgeting doesn’t have to be complicated. The 50/30/20 rule is an easy framework that can help you take control of your finances and plan for the future. By spending 50% on needs, 30% on wants, and saving 20%, you create a balanced financial plan that supports both your current lifestyle and your long-term goals. The most important step is simply starting. Even small improvements in how you manage money today can lead to greater financial stability tomorrow.

Read More →

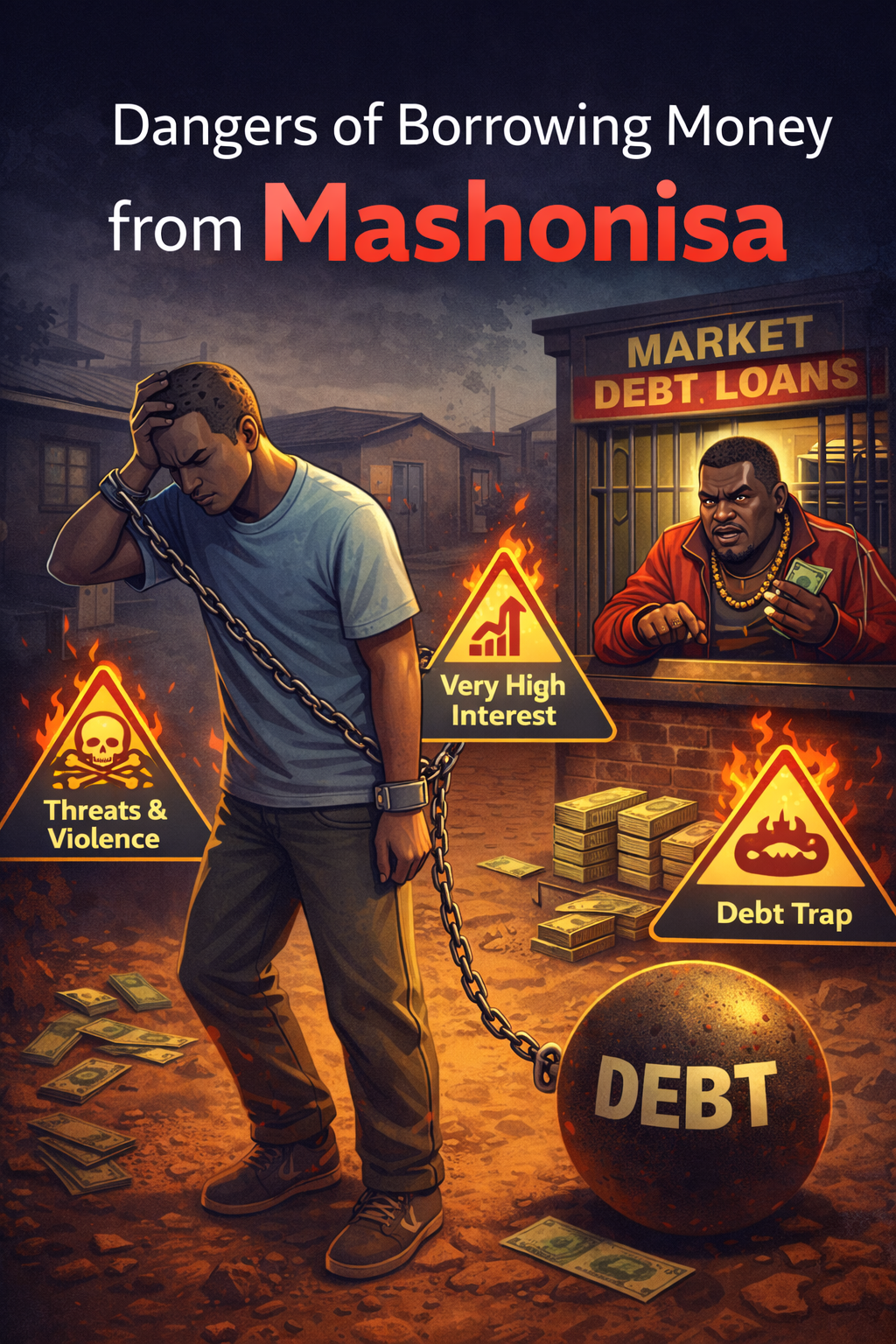

The Dangers of Borrowing from Mashonisas in South Africa (and Safer Alternatives)

The Dangers of Borrowing from Mashonisas in South Africa (and Safer Alternatives) In many South African communities, especially where access to formal credit is limited, people sometimes turn to informal lenders known as “mashonisas.” These lenders may offer quick cash with minimal paperwork, but borrowing from them can carry serious financial and legal risks. Understanding these risks can help borrowers make safer choices and protect themselves from debt traps. What Is a Mashonisa? A mashonisa is an informal money lender who operates outside the regulated credit system. They typically offer small, short-term loans but often do so without being registered with the National Credit Regulator. Because they are unregulated, mashonisas usually do not follow the rules set out in the National Credit Act, which was created to protect consumers from unfair lending practices. The Major Risks of Mashonisa Loans 1. Extremely High Interest Rates Many mashonisas charge very high interest rates, sometimes 30% to 50% per month or more. By comparison, regulated lenders must follow legal interest limits set by the National Credit Act. These caps help prevent borrowers from falling into unmanageable debt cycles. 2. Illegal Retention of ID or Bank Cards One common practice is demanding: Your ID document Your ATM card Your bank PIN This practice is illegal and dangerous. It gives the lender control over your bank account and can lead to unauthorized withdrawals. 3. Harassment and Intimidation Because mashonisas operate outside legal frameworks, some borrowers experience: Threats or harassment Public shaming Aggressive debt collection Registered credit providers must follow strict debt collection rules and cannot intimidate or abuse borrowers. 4. No Consumer Protection When you borrow from a mashonisa: There is usually no written credit agreement You may not know the true cost of the loan There is no formal dispute process Regulated lenders must provide a pre-agreement quotation and full cost breakdown before you accept a loan. 5. Debt Traps Because of high interest and short repayment periods, borrowers often end up borrowing repeatedly just to pay previous loans, creating a cycle of debt. Safer Alternative: Borrow from Accredited Credit Providers Instead of using informal lenders, borrowers should consider registered credit providers regulated by the National Credit Regulator. Registered lenders must: Follow interest rate limits Perform affordability assessments Provide clear loan agreements Protect consumer rights Example: TholaCash Financial Services TholaCash Financial Services is an example of a regulated lender that follows South African credit laws. Responsible lenders like TholaCash typically provide: Transparent loan terms Legal interest rates Secure payment systems Clear repayment schedules Customer support and dispute processes Borrowers also receive a formal quotation showing the full cost of credit before accepting a loan. Tips for Borrowing Safely in South Africa Before taking any loan, consider the following: Always check if the lender is registered with the National Credit Regulator Never give anyone your bank card or PIN Read the loan quotation carefully Make sure you can afford the repayments Avoid lenders who refuse to provide a written agreement Final Thoughts While mashonisas may appear convenient when you need money urgently, they often expose borrowers to high interest rates, intimidation, and financial risk. Choosing a registered and responsible lender, such as TholaCash Financial Services, helps ensure that your loan is transparent, fair, and protected by South African law.

Read More →What Our Customers Say

"Quick and simple process. Got my funds when I needed them."

— Sarah M."Clear repayment breakdown and very professional service."

— David K."Application took minutes. Highly recommended."

— Lerato N.