The Dangers of Borrowing from Mashonisas in South Africa (and Safer Alternatives)

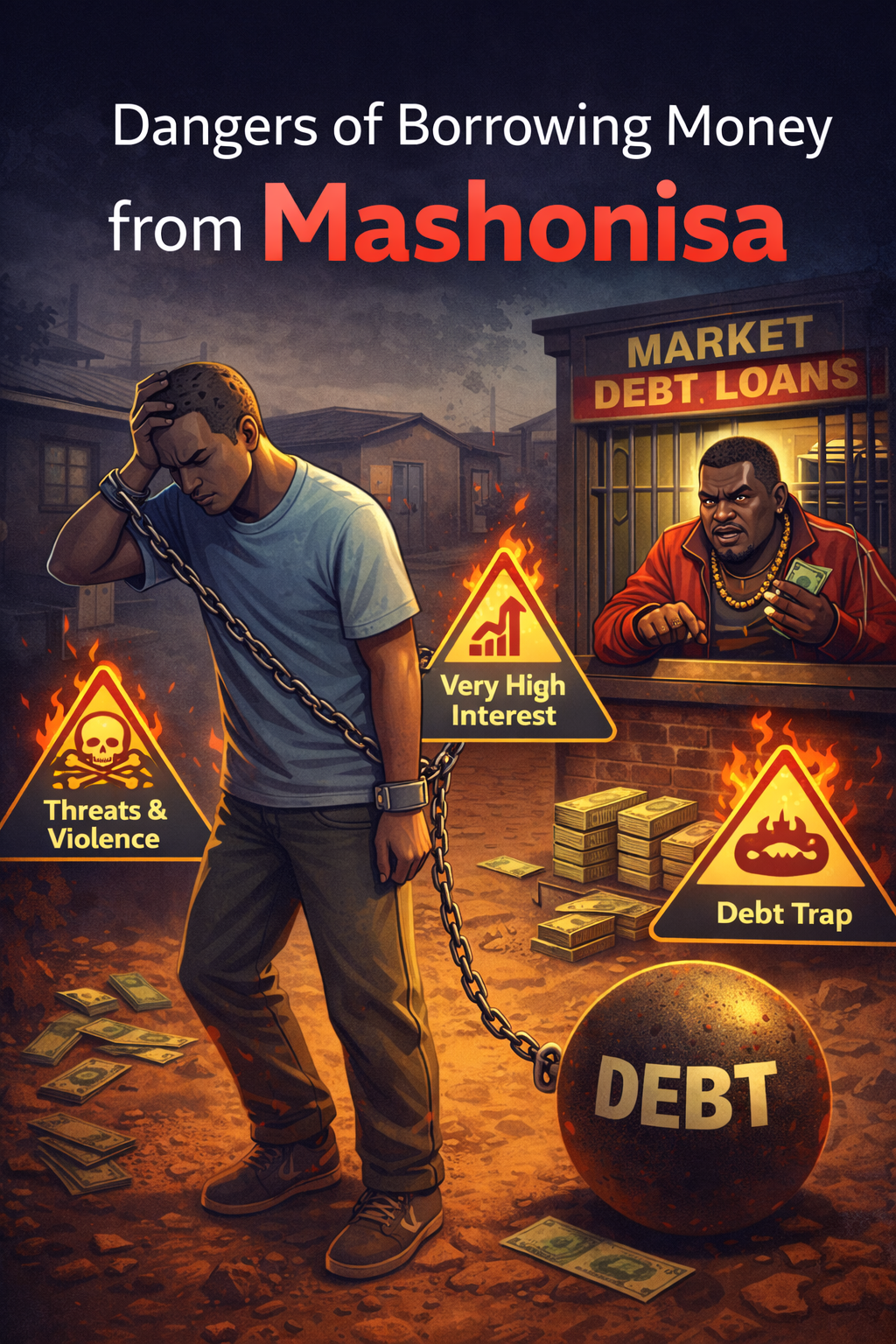

The Dangers of Borrowing from Mashonisas in South Africa (and Safer Alternatives) In many South African communities, especially where access to formal credit is limited, people sometimes turn to informal lenders known as “mashonisas.” These lenders may offer quick cash with minimal paperwork, but borrowing from them can carry serious financial and legal risks. Understanding these risks can help borrowers make safer choices and protect themselves from debt traps. What Is a Mashonisa? A mashonisa is an informal money lender who operates outside the regulated credit system. They typically offer small, short-term loans but often do so without being registered with the National Credit Regulator. Because they are unregulated, mashonisas usually do not follow the rules set out in the National Credit Act, which was created to protect consumers from unfair lending practices. The Major Risks of Mashonisa Loans 1. Extremely High Interest Rates Many mashonisas charge very high interest rates, sometimes 30% to 50% per month or more. By comparison, regulated lenders must follow legal interest limits set by the National Credit Act. These caps help prevent borrowers from falling into unmanageable debt cycles. 2. Illegal Retention of ID or Bank Cards One common practice is demanding: Your ID document Your ATM card Your bank PIN This practice is illegal and dangerous. It gives the lender control over your bank account and can lead to unauthorized withdrawals. 3. Harassment and Intimidation Because mashonisas operate outside legal frameworks, some borrowers experience: Threats or harassment Public shaming Aggressive debt collection Registered credit providers must follow strict debt collection rules and cannot intimidate or abuse borrowers. 4. No Consumer Protection When you borrow from a mashonisa: There is usually no written credit agreement You may not know the true cost of the loan There is no formal dispute process Regulated lenders must provide a pre-agreement quotation and full cost breakdown before you accept a loan. 5. Debt Traps Because of high interest and short repayment periods, borrowers often end up borrowing repeatedly just to pay previous loans, creating a cycle of debt. Safer Alternative: Borrow from Accredited Credit Providers Instead of using informal lenders, borrowers should consider registered credit providers regulated by the National Credit Regulator. Registered lenders must: Follow interest rate limits Perform affordability assessments Provide clear loan agreements Protect consumer rights Example: TholaCash Financial Services TholaCash Financial Services is an example of a regulated lender that follows South African credit laws. Responsible lenders like TholaCash typically provide: Transparent loan terms Legal interest rates Secure payment systems Clear repayment schedules Customer support and dispute processes Borrowers also receive a formal quotation showing the full cost of credit before accepting a loan. Tips for Borrowing Safely in South Africa Before taking any loan, consider the following: Always check if the lender is registered with the National Credit Regulator Never give anyone your bank card or PIN Read the loan quotation carefully Make sure you can afford the repayments Avoid lenders who refuse to provide a written agreement Final Thoughts While mashonisas may appear convenient when you need money urgently, they often expose borrowers to high interest rates, intimidation, and financial risk. Choosing a registered and responsible lender, such as TholaCash Financial Services, helps ensure that your loan is transparent, fair, and protected by South African law.